It looks like we’re going to head into the weekend on an upbeat note thanks largely to, i) bank earnings, and ii) China PPI.

Below, find a bit of Street commentary on results from JPMorgan, Citi, and Wells Fargo courtesy of Bloomberg:

From Goldman’s Richard Ramsden:

-

JPM

-

Strong FICC rev. drives beat

-

Total rev. outperformance driven by FICC, investment banking, “slight” NII beat

-

Neutral/attractive, PT $71

-

-

C

-

Better FICC drives beat

-

Card growth, reserves “inflecting”

-

C continued to benefit from Costco acquisition, as expected, with accelerating global sales, ANR, rev.; notes ex. Costco in North American, card rev. +1%, first time C’s had positive underlying rev. since before 4Q 2014

-

Notes added $400m in reserves in NA consumer bank to provide for growth

-

Neutral/attractive, PT $50

-

-

WFC

-

Results in line; concern about sales practices overhangs

-

Buy/attractive, PT $51

-

From Guggenheim’s Eric Wasserstrom:

-

JPM

-

Operating trends better than recently-reduced expectations, suggesting upside to 2016, 2017 EPS ests.

-

Neutral

-

-

C

-

Operating rev. beat driven by higher noninterest income on strong y/y results in fixed income trading

-

NII trailed on lower NIM, lower earning assets; expenses higher; provision lower, driven by lower NCOs

-

Results suggest upside to 2016, 2017 EPS ests.

-

Buy

-

-

WFC

-

Legal, remediation costs likely to undermine asset growth, creating downside risk to 2016, 2017 ests.

-

3Q reflected weaker NII vs est. on lower NIM, which offset stronger loan growth (driven by C&I, CRE and consumer); notes mortgage banking rev. beat ests.

-

Neutral

-

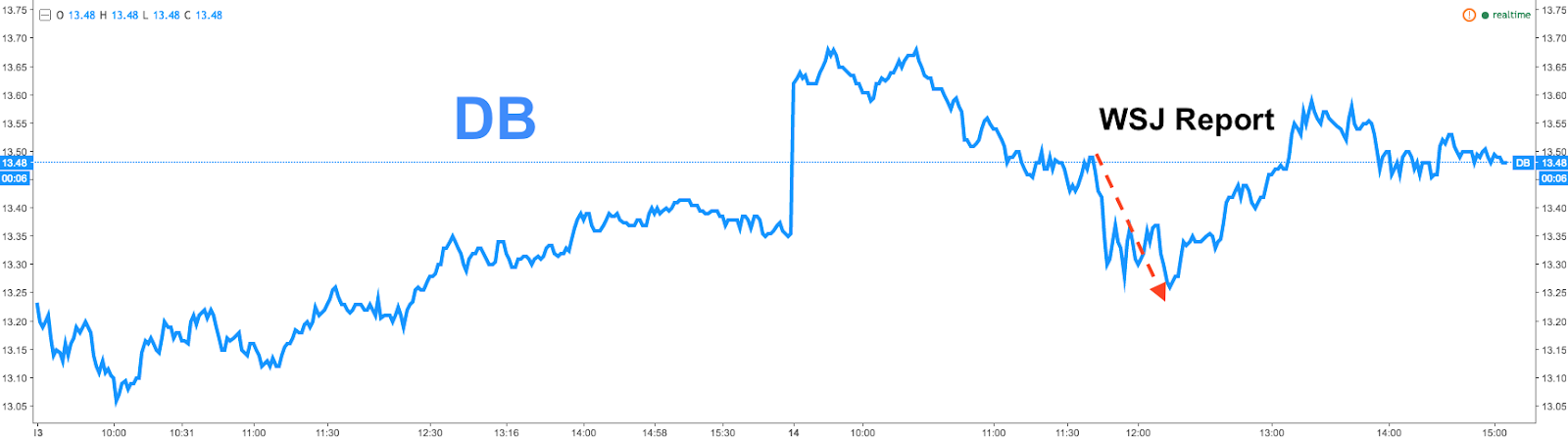

Still, sentiment in the space is sour thanks in no small part to the ongoing drama at Deutsche Bank which, quite frankly, may ultimately go the way of Lehman. Shares rose early this morning but green turned to red around lunchtime eastern when WSJ reported that the German government apparently isn’t feeling as benevolent towards the country’s largest lender as it is towards Syrian refugees. Here’s an excerpt:

“Aides to German Chancellor Angela Merkel have told lawmakers the state wouldn't take a stake in Deutsche Bank AG if it were to issue new stock to shore up its thin capital cushion, one person who attended the briefing said.”

“The fact that Berlin appears to have ruled out any aid for the embattled lender as both unnecessary and politically unfeasible could put Deutsche Bank under renewed pressure as it works to stabilize its share price and stay out of the news while negotiating an acceptable settlement in a U.S. misconduct investigation.”

Then, a couple of hours later, we got this:

DEUTSCHE BANK SAID TO DISCUSS REDUCING U.S. PRESENCE: SZ

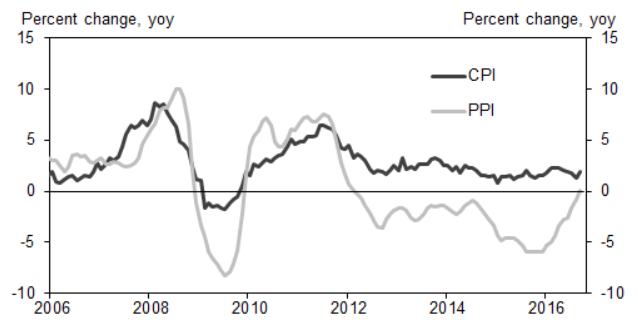

As for China PPI, if you believe the NBS (which you probably shouldn’t) factory gate prices rose for the first time in half a decade last month thanks largely to metal and coal. Here’s a visual:

(Chart: Goldman)

But not so fast, Goldman says. This may be attributable to easy compares:

“Our analysis suggests that the recent sequential pickup of headline PPI in 2016 has been due primarily to a depreciation of the RMB and recovery of oil prices. In addition, favorable base effects (falling oil prices over the course of 2015) have contributed to a moderation in year-on-year PPI deflation.”

What’s also interesting to note here is that China has arguably been able to artificially prop up its GDP by tying the deflator more closely to PPI than it should. That is, the NBS just uses PPI as the deflator which, in times of falling commodity prices, allows Beijing to overstate economic output. So what happens if/when PPI begins to rise?

Anyway, that’s speculation. The point is, we got the right recipe to end the week on a positive note, but this will likely be fleeting. As we’ve outlined previously (and at length in our latest e-book), there are too many landmines out there to count, although the Trump allegations have admittedly removed some uncertainty from the equation (no matter who you’re voting for, short-term volatility will almost certainly spike if Trump were to come out ahead).

Meanwhile, Janet Yellen took to talking out of both sides of her mouth Friday afternoon when, at a Boston Fed conference, the chair suggested that an overheating economy might be the best prescription for the damage inflicted by the recession while at the same time acknowledging that “lower for longer” could lead to hyperinflation (she obviously didn’t use that term, but it’s what she meant) and financial asset bubbles.

So that’s your Friday recap.

To be frank, it feels quiet out there. We’ll see how long that lasts.

1 Comment

[…] For more, see here […]