It seems pretty clear that markets are not going to cooperate with the Bank of Japan.

Recall that earlier this week, Haruhiko Kuroda announced the bank would begin managing the yield curve in an apparent effort to steepen things up a bit so the country’s banks don’t shrivel up and die. Here’s a look at the curve:

The BoJ also committed to “overshooting” its inflation target.

Much like the initial foray into negative rates back in January, traders are apparently prepared to test policymakers’ resolve. Have a look at the the yield on Japanese 10s:

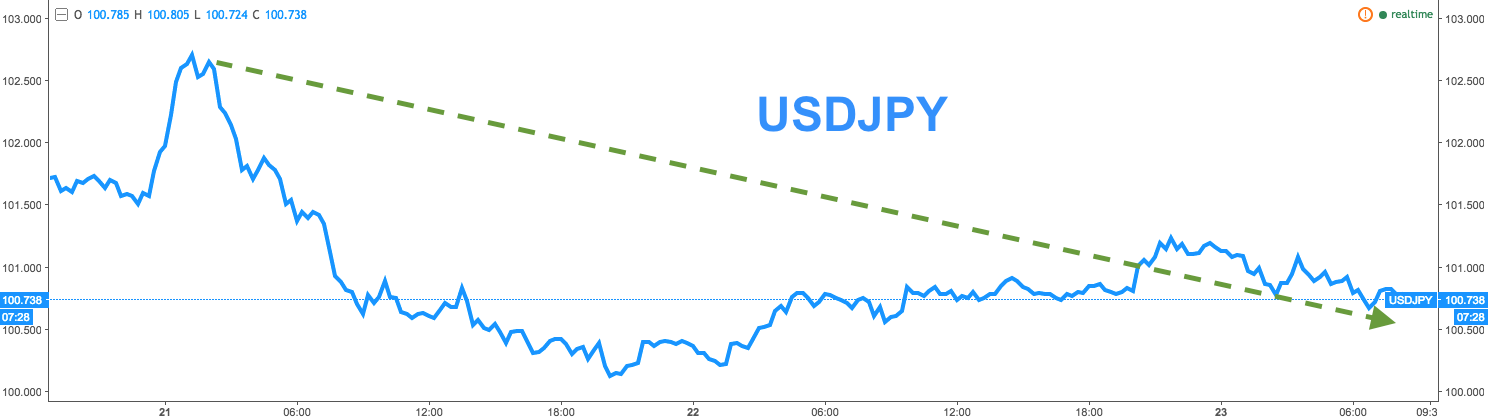

And here’s the yen:

Note what’s happening here. This is once again an example of the market doing the exact opposite of what the BoJ intends to bring about. Yields on the 10 are ticking lower and the currency is getting stronger. Here’s WSJ:

“In a further sign of the challenge now facing the Bank of Japan with its self-styled new policy of ‘yield curve control’, prices for government bonds of different maturities on Friday moved in ways that run counter to its aims.”

“The yield curve instead flattened slightly during the day: the yield on shorter-term bonds, such as the 2-year tenor, rose slightly, while the yield on Japan’s newest 20-year bond was trading at 0.375% compared with 0.415% on Wednesday.”

“Banks won’t benefit much from the BOJ’s yield-curve control policy unless 3-5 yr yields rise,” Japan Post Holdings CEO Masatsugu Nagato said today, adding that implementation of the new policy will be a “major challenge” even as he said Kuroda is “doing a great job.”

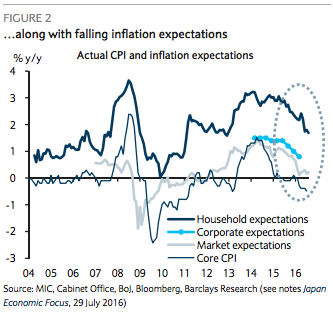

We suppose this is what a “great job” looks like on the inflation front:

(Chart: Barclays)

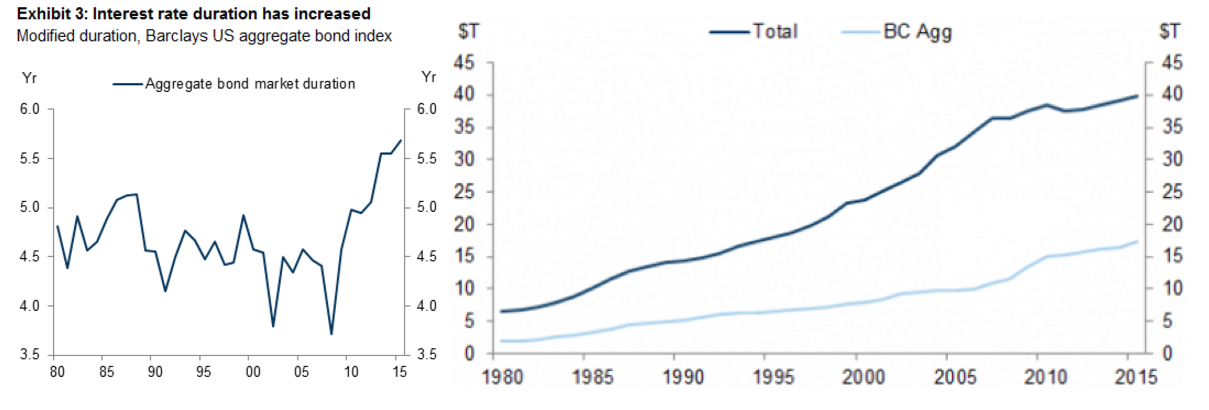

Perhaps the market’s reluctance to cooperate is a blessing in disguise. After all, we can estimate that a 100bps move to the upside in yields on US bonds would lead directly to between $1 and $2.5 trillion in losses thanks to exploding debt and rising duration risk:

(Chart: Goldman)

One could expect a similar bloodbath if we saw a sharp backup in Japanese government bond yields - i.e. if the BoJ mismanages things. As WSJ notes, “uncertainty about the central bank’s buying could make market participants less willing to subscribe in future auctions for new government bond issues,” meaning markets could be “underestimating the effect on liquidity,” according to Citi’s Thomas Reich.

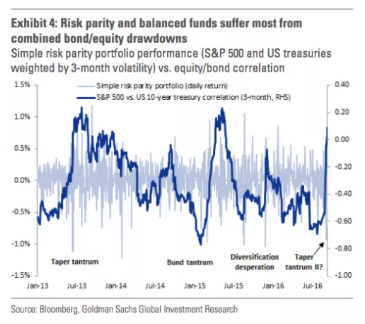

Now have a look at the bond/equity correlation (dark blue line):

(Chart: Goldman)

It hasn’t been this elevated since the German bund tantrum. In short, if the Bank of Japan ends up overshooting its target level of around zero percent for the Japanese 10Y or otherwise creates a situation (e.g. soft demand at auction) where yields are susceptible to a big move to the upside, watch out, because your stocks are going to suffer the same fate as your bonds thanks to the many risk parity strats that will be forced to unwind everything.

1 Comment

[…] general consensus is that this is doomed to fail and as we discussed earlier today, there’s a pretty high likelihood that they make a mistake. Throw in the fact that the yen is […]