The U.S. economy is in an interesting situation. The manufacturing economy started weakening in 2014. Industrial production has declined for 13 straight months which is the longest streak outside of a recession ever. Earnings peaked in 2015 and have been declining ever since. Both the Russell 2000 and the NYSE peaked in 2015. All of these stats line up with a recession in 2016 where the late-cycle indicator which is employment starts to deteriorate and the major indices (the S&P500 & NASDAQ) fall into a bear market.

This decline in the labor market and stock market hasn’t happened yet. While one can explain the extending of this very weak recovery by saying every economic cycle is different, this would ignore the role the central banks have played. The best way to describe current monetary policy is a grand experiment to see how assets appreciating will affect the overall economy. Even without a nasty recession, the results are not good as the US economy has had a long benign recovery.

The expectations for earnings to rebound in 2017 assume the economy has gone through the weak period and will get back to growing at the 2% it had seen before it started to decelerate in late 2015. Even though Goldman Sachs lowered its 2017 earnings expectations today, it still is projecting 10% EPS growth for the S&P 500. Normally at this point in the cycle the employment picture would be weakening to the point where Goldman would be able to project a decline in earnings which would likely end up having to be revised lower because Goldman is in the sales business and always has to have a positive spin to help its business. In this current case the length of the end of the cycle makes future earnings estimates more disjointed from reality than they would ordinarily be.

While the possibility that the worst is over for the economy and earnings recession exists, I don’t consider it likely. I would go as far as to say that Goldman’s projections for the next few years are virtually impossible as it is projecting earnings growth in 2018 to grow 5% and 4% in 2019. The reason why I see this endless growth phenomena as unlikely is because of the debt the global economy has racked up trying to get growth to re-accelerate after the previous recession.

The chart above shows the global debt as percent of GDP being at its record high. The previous recession was quelled by the big fiscal spending stimulus packages especially in China. There never was a proper deleveraging. The debt level will likely rise higher in the near future as tax payments lower as corporate profits have been declining. Part of the reason for earnings optimism in 2017 is the bet on a fiscal stimulus. Those betting on this possibility must be ignoring the chart above. I don’t see fiscal stimulus as likely. I see a deleveraging finally occurring. This would be healthy and allow for the future recovery to be stronger than this current one.

The best description of the current bifurcation of stocks and economic weakness is Caterpillar. Investors buying Caterpillar are buying into the fiscal stimulus led recovery in 2017 fantasy I explained. The chart below shows how bad sales at Caterpillar are as updated sales were released today. Worldwide retail sales declined 18% in the past three months. Retail industry sales fell 37%, retail construction sales fell 10%, and energy and transportation sales fell 25% (all in the past 3 months). This is while Caterpillar stock is near its 52 week high.

The one chart which explains this entire situation is the balance sheet of the 10 largest central banks shown below. These asset purchases are what allow the global debt to be at the highest in history and stocks to simultaneously rally. This chart is the only logical explanation for why Caterpillar stock is so high. The question to when this situation will reverse is answered by when the faith in central banks ends. This may come when a fiscal stimulus isn’t enacted and US corporate earnings decline because of the strong dollar and bulls have to admit the only thing holding up equities is the funny money printed at the Fed.

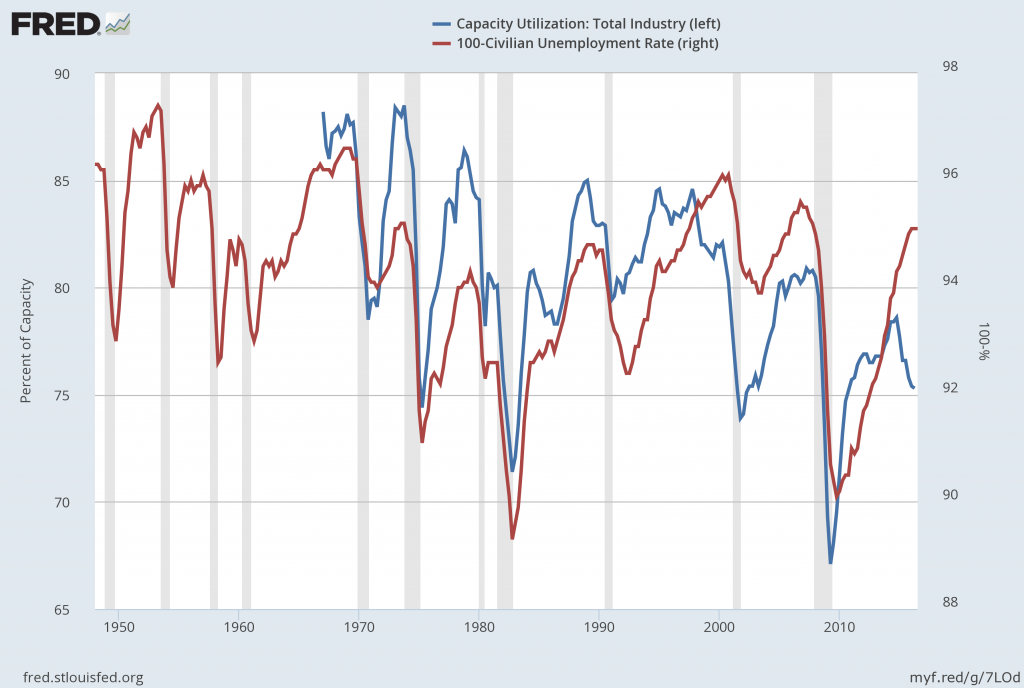

The final chart I will leave you with is the historical chart of the capacity utilization rate compared with the unemployment rate. Capacity utilization shows the historical production versus demand in the economy. Ordinarily there is a business cycle with growth occurring when demand exceeds production and recessions happening because of over-production. The current cycle peaked in November of 2014. We have experienced a decline in the capacity utilization, but, as I said, I don’t think the cycle has bottomed because of the enormous global debt which has to unwind. A further decline must be paired with an increase in the employment rate. It is almost impossible for firms to not lay off workers with their margins declining so quickly.

Conclusion

There are a few uncertainties and a few certainties I have about risk assets and the economy. I am certain the balance sheet of central banks will continue to accelerate. I am certain the capacity utilization has peaked for the cycle and that further declines will be met with an increase in the unemployment rate. I am also certain fiscal stimulus would increase the debt which will be terrible for the long term health of the economy. What I am not certain of is how this correlates into asset prices. Junk bonds have ignored increasing defaults and equities have ignored declining earnings. The question is how long this can last.