Stability Ends For Stocks As Politics Causes Modest Volatility

On Tuesday, the S&P 500 fell the most in 1 month. Mostly because House Speaker Nancy Pelosi announced an impeachment inquiry. It caused stocks to fall probably because of the uncertainty of the situation. Democrats control the House and the GOP controls the Senate. Which makes it unlikely that President Trump will be removed from office.

We’re seeing some investors compare this situation to 1998 when President Clinton was impeached. In that situation stocks initially fell and then rallied sharply. We got the initial decline on Tuesday as the S&P 500 fell 0.84%. It finally ended its streak of 13 days within 1% of 3,000. That’s not how many investors expected the streak to end.

An issue with the comparison with 1998 is that the impeachment isn’t why stocks rallied. A stock market rally like the late 1990s is unlikely since that was the greatest bubble in American history. No, stocks won’t rally because of the impeachment. That example simply shows us the impeachment isn’t a reason to sell stocks. How can this political event effect S&P 500 earnings? It probably won’t.

The Democratic primary matters more. October debates will have 12 candidates which might make them irrelevant because the top candidates might not debate each other. A main question is whether Biden and Warren go on the same night. They will go head to head with fewer competitors in the November debate because the threshold to make the debate has been raised from 2% in the polls to 3%.

Specifics Of Tuesday’s Action

Nasdaq fell 1.46% and Russell 2000 fell 1.58%. VIX was up 2.14 to 17.05. Personally, I think the VIX is too high. Impeachment inquiry threats shouldn’t cause a sharp decline in stocks. Especially because it probably won’t lead to Trump’s removal.

CNN fear and greed index fell 5 points to 54 which is neutral. Every sector fell except consumer staples and utilities which were up 0.23% and 1.06%. This was a classic risk off trading session. Worst 2 sectors were communication services and energy which declined 1.34% and 1.63%. Much of the energy sector’s gains from late August to early September have been given back.

"Impeachment inquiry" was the perfect excuse for treasuries to continue their recent rally. Yields have dropped sharply since their peak earlier this month. 10 year yield is only at 1.65% which is 25 basis points below its peak this month and only 22 basis points above its high this year. Both the high and the low were made this summer, showing how quickly the movement occurred. A recent decline in the long bond will help the housing market regain strength. It should have a very good fall.

2 year yield is only at 1.61% which is 19 basis points below its month high and 18 basis points above its year low. This decline in short yields increased the odds of a cut this year. Odds of a cut in 2019 increased to 77.6%. Personally, I see the cut as more likely to occur in December than October, but we will see. It would be a big switch for the Fed to go from calling for no more cuts at its September meeting to cutting in October.

Housing Price Growth Actually Improves

For the first time in years, the FHFA home price index’s growth rate actually improved in July. It went from 4.8% to 5% which beat estimates for 4.6%. Monthly growth increased from 0.2% to 0.4% which doubled estimates. Outside of June’s reading, this was still the weakest growth rate in almost 4 years. Strongest region was the Mountain states. They had 7.6% yearly growth and the weakest was the Middle Atlantic which had just 3.6% growth.

Core Logic Growth Rate Hits A 7 Year Low

It was tough for investors to make any vast proclamations about the FHFA report. Mostly because the growth rate in the July Case Shiller index was the weakest since September 2012. Decline in price growth is moderating because of the decline in interest rates and the easier comparisons. Barring sharp weakness in the labor market, housing price growth is very close to its bottom.

Specifically, yearly growth fell from 3.24% to 3.18%. Rounded, that’s no change. On the one hand, the 2 year growth stack fell more than yearly growth since the comp went from 6.2% to 6%. On the other hand, comps will continue to get much easier. It’s a one way trip down as December’s yearly growth rate was 4.6% last year. I can’t see how yearly growth falls much further with these easier comps and rates near their all-time low.

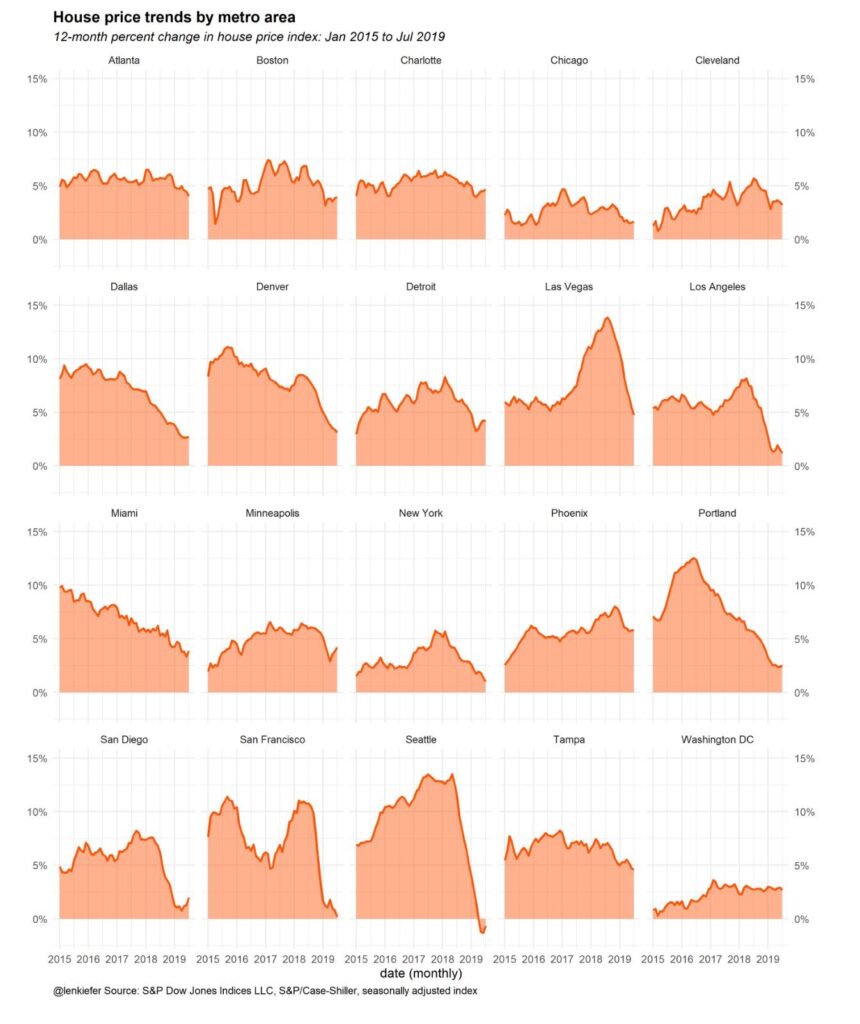

Just like last month, the 20 city growth rate was much worse than national price growth. Seasonally adjusted monthly growth was 0% which was the same as June and missed estimates by 0.1%. Non-seasonally adjusted yearly growth was just 2% which fell from 2.2% and missed estimates by 0.1%. The charts above show the growth trends in each city.

Yearly price growth in Seattle actually bottomed as it increased from -1.3% to -0.6%. That’s what happens when the comp falls from 12.8% to 11.5%. The comp is going to keep falling which means it should see low single digit positive growth soon. Las Vegas saw a sharp decline in growth because it peaked later than Seattle. It peaked in August of last year.

Growth in July fell from 5.5% to 4.7%. Once again, Phoenix had the highest growth rate as it fell about 1 basis point to 5.8%. That’s impressive, because it also peaked late as its growth rate peaked in November 2018.

Conclusion

I’m not concerned with the impeachment proceedings as an investor. But I will do my best to cover any big news items in an objective way. Decline in house price growth in the Case Shiller index helps affordability. Although technically average weekly wage growth was 2.7% in July which is below home price growth.

A main driver of affordability gains is rates. Since weekly wage growth increased to 2.9% in August, home price growth could fall below weekly wage growth in the next report.

Recent Comments