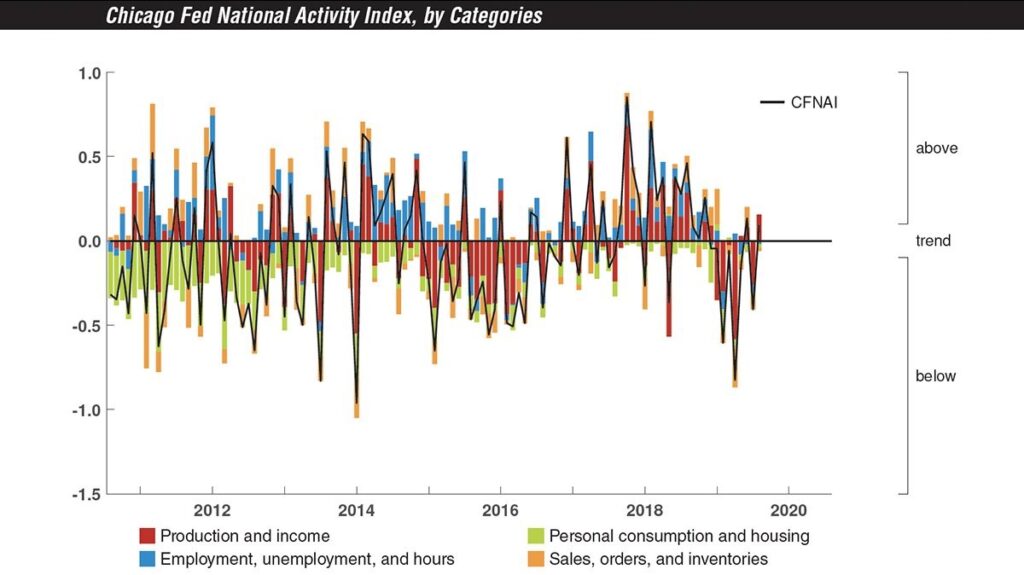

Positive National Chicago Fed Reading

Bears love to pick out the negative readings in the national Chicago Fed index and use them as evidence for a recession forecast. Anyone who has followed this report for a few months knows that’s not the correct way to look at it. Firstly, negative readings are common. Secondly, even big negative readings can be revised positively. It’s best to review the 3 month moving average and not to overreact to one month of data.

August readings were solid. Revisions in this report were mixed. June reading went from 3 basis points to 13 basis points and the July reading went from -36 basis points to -41 basis points. A terrible April reading you can see in the chart below remained. At this point, we can look past such a reading because the weakness clearly didn’t persist. Revisions didn’t change the 3 month average which was -14 basis points in July.

August index was relatively solid. It improved to 10 basis points. This pushed the 3 month average to -6 basis points. It’s good to see an improvement, but this was the seventh straight negative reading. It’s clear the economy is in a modest slowdown. 3 month average is nowhere near a recessionary reading which is -0.70.

The August report was helped by industrial production and hurt by the ISM PMI. This report showed broad shallow weakness. Employment, sales/orders/inventories, consumption, and housing all had marginal declines of 0.2. 51 of the 85 indicators in this report were included in the August reading. The fact that so many indicators aren’t in the initial reading explains why revisions are often so sharp.

Negative Markit PMI Shows Life

In my opinion, the September flash Markit PMI was good because it showed improvement. We keep expecting a shoe to drop, but economic data has recently been solid. Now with this Markit report, it’s not just housing data coming in ok. The Markit PMI was at the heart of many bearish calls. It’s not exactly bullish now, but there is less recession risk. Specifically, the composite PMI improved from 50.7 to 51 which is a 2 month high. Generally, you don’t see new highs in PMI data in a recession or near a recession.

Improvement in the composite PMI was driven by both services and manufacturing. Services PMI improved from 50.7 to 50.9 which is a 2 month high. Manufacturing PMI increased from 50.3 to 51 which is a 5 month high. Output index also hit a 5 month high as it increased to 51.7 from 50.8. This improvement is in line with the recent solid monthly growth in the August industrial production report. Weakest part of the economy is showing improvement in rate of change terms.

Bad news is because the services index missed estimates by 0.5, the composite index missed estimates by 0.2. Furthermore, as the chart above shows, the PMI is consistent with about 1.5% Q3 GDP growth which is below the consensus of 2% growth. Worst part of this report was the employment reading. Service sector had a reduction in employment numbers for the first time in almost 10 years. This resulted in the Markit report being consistent with less than 100,000 jobs created per month. This means job creation could fall below the amount necessary to keep up with population growth.

Job growth has been weakening all year as you can see from the chart below. It hasn’t yet weakened to the point where it has hurt consumer spending as PCE growth was great in Q2 and August retail sales growth was great. This report should make investors keep a watchful eye on jobless claims and the September labor market report.

Markit report often mentions how this was a historically weak report that showed modest improvement. However, considering the recession fears, I see any improvement as a win. Composite PMI is below the 10 year average of 55. Rate of new private sector business growth was the weakest since October 2009. Business expectations improved slightly from the 7 year low hit last month. It’s interesting that the latest trade news didn’t make firms more pessimistic. Just like the composite index, the service sector had the weakest new work growth since October 2009. Input costs fell the most since late 2009.

Moving to the manufacturing sector, output and new order growth drove the index higher. There was a small increase in employment. Export orders were weak again as international new work fell for the 4th time in 5 months. Purchasing activity and pre-production holdings fell. Stock of finished goods also fell. If the increase in new work continues, this will need to reverse. Inflation accelerated for inputs and output which makes sense since the PMI improved modestly.

American Manufacturing Outperforms Germany

The chart below gets at the point I have been making. Yes, the data isn’t great, but it isn’t as bad as it could be. This data isn’t recessionary and is headed in the right direction. As you can see, despite the strong dollar and trade war with China, the US manufacturing PMI increased while the German PMI fell from 43.5 to 41.4 which is a new cycle low.

This was the worst PMI since 1996 outside of the 2008 financial crisis. Results aren’t better when you look at all of Europe. Composite PMI fell from 51.9 to 50.4 which is a 75 month low. Services PMI fell from 53.5 to 52 which is an 8 month low. Finally, the manufacturing PMI fell from 47 to 45.6 which is an 83 month low.

Conclusion

Chicago Fed National Activity index and the Markit PMI both showed sequential improvement and that the slowdown is still in place. Unlike the recent housing reports, the Markit composite PMI missed estimates. It also had a weak employment reading.

US manufacturing sector is nowhere near as weak as Europe’s which is deep in recessionary territory. American manufacturing PMI was actually above its services PMI.

Recent Comments