The long term consequences of the Fed’s policy mistakes are obvious. Low interest rates created the tech and real estate bubbles, so having interest rates lower for longer is going to cause more damage. We are already seeing these effects bear fruit as the S&P 500’s median price to sales ratio is the highest ever. Stocks are expensive because bond yields are low. Low government bonds have also caused junk bonds to be 2 standard deviations more expensive than they should be.

The factors have been known for years as quantitative easing has boosted valuations. However, whenever a bear mentions that stocks are overvalued, bulls argue that this situation will continue. The bulls have been correct ever this year as the economic data has sagged lower than ever, but stocks have stayed at this current plateau.

The Fed can decrease its balance sheet and raise rates to pop the bubble, but bulls argue this won’t happen. If the Fed controls the bubbles, can’t they last forever? The answer to that will be explained in this article.

Before I explain the two problems which will occur in the near term if the Fed stays put like it has been doing this year, I will review the Fed’s policy. The Federal Reserve is undergoing an “all talk, no action” interest rate policy. The Fed cannot raise rates because it will burst the bubble in stocks, bonds, and real estate as I said previously. However, the Fed cannot tell investors it will never raise rates because that would cause assets to rise hyperbolically and encourage intense criticism from the public, financiers, banks, and the media. Therefore, the Fed says it will raise rates and then doesn’t do so. Having hawkish forward guidance also allows the Fed to ease conditions if there is financial tightness. It’s akin to having the unlimited ability to cut rates even though they aren’t changing.

Having interest rates this low causes the system to buckle even without the bubbles bursting. The consequences are far reaching. On consequence is pension funds being in a poor position to meet obligations because they can’t get returns on fixed income. The result is an increased exposure to stocks. Even with this increased exposure, pension funds are in worse shape than they were in 2008.

If pension funds can’t meet obligations, then they have to cut payouts or get bailed out. A bailout of pension funds would be the equivalent of the Fed plugging the holes of a sinking ship. Part of the problem is stock prices. Stock prices remaining slightly above the price they were 2 years ago is causing problems which would cause them to go down which would start a virtuous cycle lower.

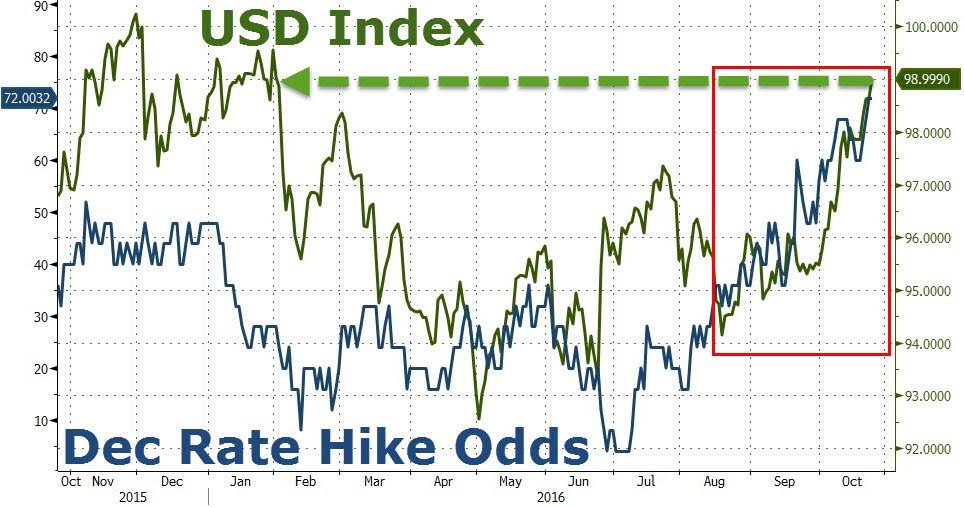

The second issue I will discuss is the rising dollar. The Fed is in a unique predicament compared to where it has been in the past few years. It has to paint a good picture of the economy to help the incumbent party look good to get Hillary Clinton elected. This means the Fed has to sound more hawkish than usual. Usually the Fed has a lot of bluster about raising rates, so the current level of bluster is so high the Fed is close to guaranteeing a rate hike. The Fed looks bad when economic data is disappointing, but it has convinced the market it will raise interest rates. As you can see from the chart below, there is now about a 70% chance of a rate hike in December. This 70% threshold is what many feel is necessary for the Fed to raise rates without spooking the market.

The problem lies in the dovishness of other central banks. The Fed is reliant on the monster it created. What I mean by this, is the Fed’s dovish policies have encouraged other central banks to try them. Now that they are all dovish, the Fed cannot exit its own policy without causing the dollar to rally. While a strong dollar is a positive, the Fed would prefer a stable dollar to one that is skyrocketing.

The Fed is only talking about a quarter point rate hike which would set the speed at one rate hike per year. This has already caused the dollar to reach 8 month highs. Imagine what would happen to the dollar if interest rates were normalized to about 2% and the Fed sold the $4.5 trillion in government bonds it owns. The dollar would rally even further.

The strong dollar hurts multinational firms’ earnings which have already been hurt by weak demand. Combining a strong dollar with an economy which is headed for a recession is a recipe for sharp earnings declines. If the Fed is able to keep stocks high, this would increase the bubble even more as valuations would be out of control.

Conclusion

Anyone who is bullish on stocks because of Fed support (which is the only reason to be bullish) needs to recognize the potential problems the Fed faces. If it continues to keep rates low, pension funds will be crimped. If it has too much bluster on raising rates, it could cause the dollar to rise too high. If there is too little bluster, market participants question whether low rates are permanent. If it actually raises rates the asset bubbles will burst.