Going into this earnings season earnings were expected to decline 2% year over year. Earnings expectations are a farce unfortunately. Analysts may have always been lowered expectations to foster earnings beats, but this practice has become painfully obvious recently because of the current environment where EPS growth has been negative while stocks have been rallying.

It’s not necessarily the analysts’ fault that the projection lies are believed by the market, but they are complicit in the situation. Sometimes algorithms push stocks higher when they beat expectations and other times stocks move higher simply because of Fed policy buoying all stocks. The fundamentals have mattered little over this period.

Earnings projections are beat by about 3% on average. Therefore my expectations for earnings in Q3 was 1% growth at the start of the quarter. You can see the farce being played out in the chart below. It shows how earnings estimates were cut in the summer to allow firms to beat estimates. As of October 25th the earnings growth has been 0.2%.

Bulls will argue that earnings growth being positive are a sign that we will return to double digit earnings growth in 2017 as the current expectations are for about 13% growth. It’s intellectually dishonest how bulls were willing to exclude energy earnings declines when they were bringing down the average, but are now including their positive rebound in 2017 estimates.

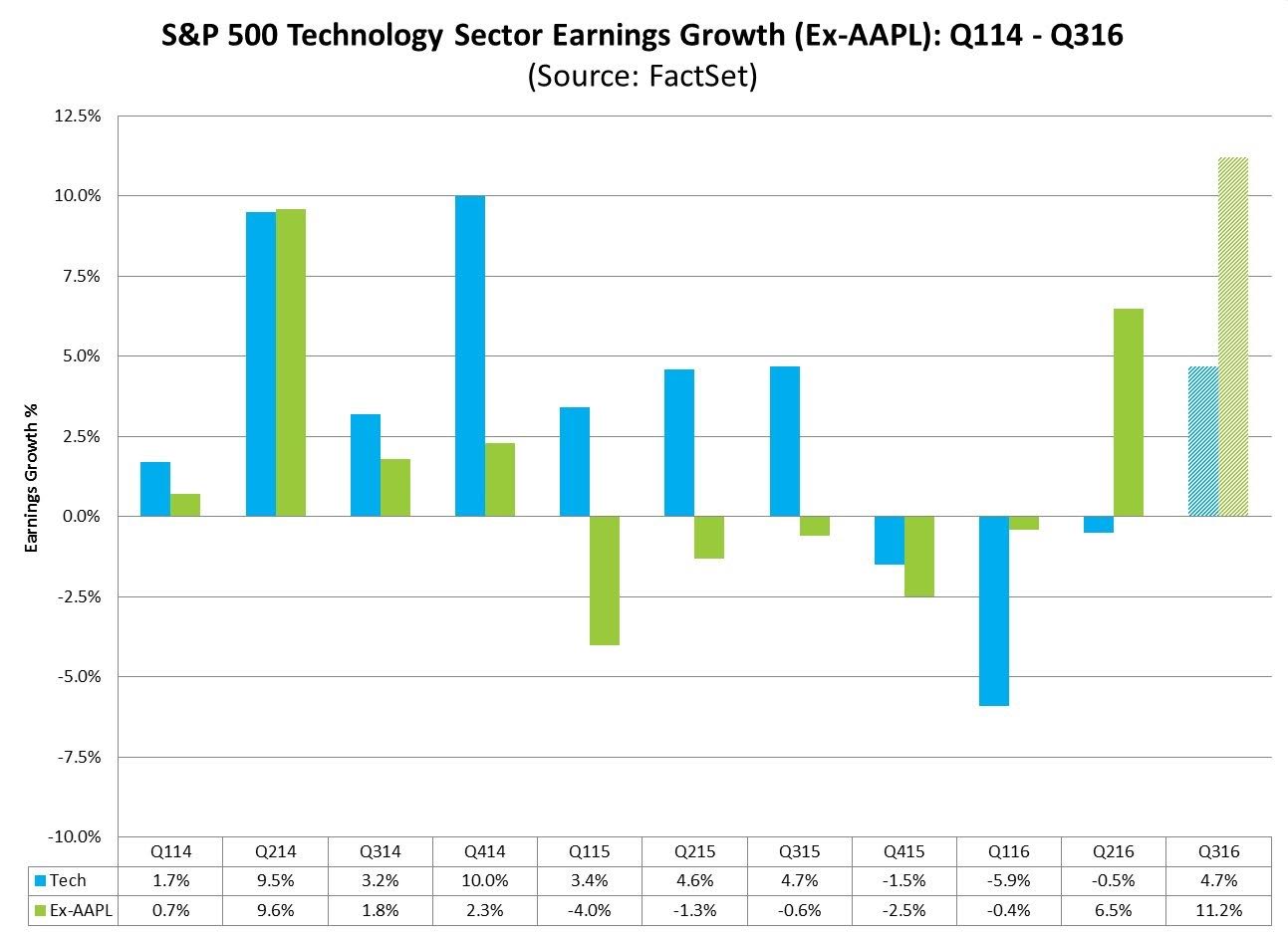

One of the biggest impacts to earnings results has been Apple. As you can see from the chart, Apple has hurt tech earnings this quarter by 6.5%. This chart is the same type of one I described with energy. Bulls are always excluding the negatives and including the positives to paint a better picture than reality. This is similar to the way Apple now plays up its services revenue which is growing consistently now that hardware has been weak. Apple had used to be able to tell the truth about its business because it was doing well. Now that Apple has become like IBM, it has to buy back stock to boost EPS as revenues decline. I wouldn’t look at Apple being weak as a positive. It is a negative because it will be a noose around the neck of tech earnings growth in the future.

Boeing is the stock that caused the Dow to rally today in the face of the NASDAQ’s decline which was caused by Apple’s decline. However, the same earnings misdirection applies to Boeing as well. EPS of $3.51 was 40% higher than last year, but this can solely be attributed to favorable tax items of $0.98. Full year guidance was adjusted higher as revenues will now be $64.5-$65.5 billion which is up from $64-$65 billion. However, this needs to be put into context because in Q1 the company provided guidance which was lower than expectations and in Q2 some metrics were lowered again. It’s not as if Boeing is beating the original expectations.

We saw the same thing from IBM earlier this month. Below I have the effective tax rate IBM has historically paid. The trend is lower as the company uses accounting gimmicks to beat consensus estimates. Revenues were $19.226 billion which beat estimates for $19.0 billion. However, this was the 18th consecutive quarter of revenue drops even as the firm makes acquisitions at a rapid pace to improve revenues.

The final example I will show is with Caterpillar. In April I remember CNBC boasting about how CEO Oberhelman said the company was nearing a bottom. This is the same guy who overbuilt capacity in 2010 and bought Bucyrus (a mining company) for $8.8 billion in 2011 which was right before the top of the market in 2012. Surely his credibility on predicting future economic results is low. However, this statement was proclaimed to be the end of the economic rut. The only thing that has ended is Oberhelman’s tenure at Caterpillar as he will step down in March of next year. You can see Oberhelman’s failures as CEO in the annotated chart below. As I referenced in my previous article, Caterpillar had to lower guidance again this quarter. The stock is actually up over 23% this year even after four straight years of revenue declines and continual guidance misses this year.

Conclusion

The earnings picture has improved moderately as Q3 will likely see a very small increase in year over year earnings of about 1%. The bulls can spin these results as the beginning of the next great rally in profit margins and stocks, but given the record high debt levels of corporations and the accounting manipulation, I will call their bluff. Given the negative earnings quarters were spun into positives, there is nothing that can get in the way of the narrative. An honest narrative would acknowledge that the Fed has been behind most of this rally, but it is losing steam because the business cycle is rolling over.