If you think it feels a bit tenuous out there you’d be right.

On the heels of a rather inauspicious Tuesday session that saw the British pound hit a 31-year low while crude and gasoline futures plunged on (over)supply concerns, it was risk-off overseas, a sentiment that muddied the waters on Wall Street ahead of the Fed Minutes. Here’s a look at the usual suspects:

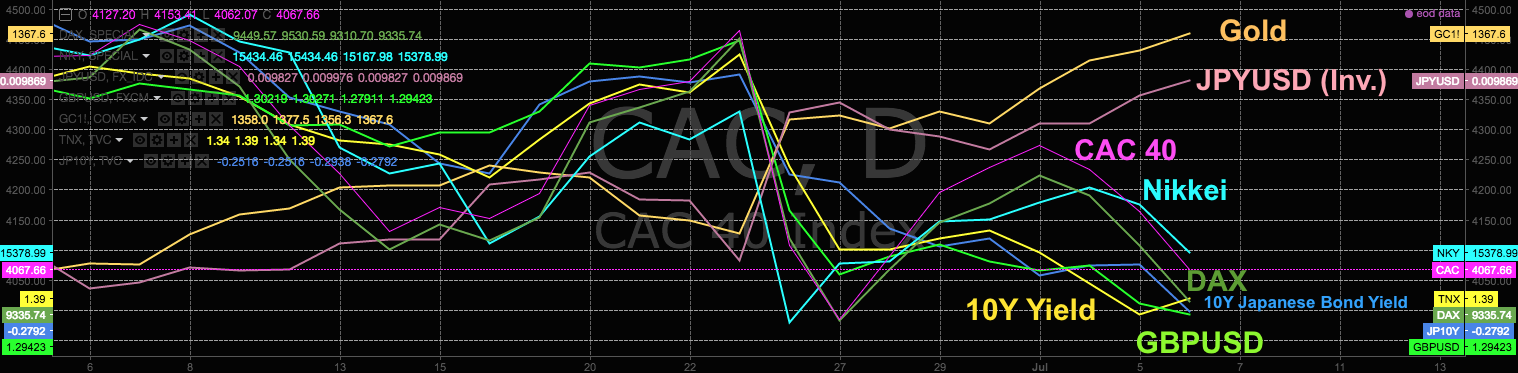

Same story. Havens were bid (yen up, gold up), stocks were weak (CAC, DAX, Nikkei), bond yields were suppressed, and the pound was in free fall. Here’s Bloomberg with the summary bullets:

-

Global stocks sink with pound as haven demand boosts bonds, gold

-

Pound takes fresh leg lower on mounting Brexit woes as yen jumps

-

Swedish central bank delays rate-increase plans

-

Yuan in longest losing streak since February as forecasts cut

Yeah. Nothing good about any of that. As of midday, US stocks managed to shake off the blues to trade green, but as noted above, it’s a shaky session. There’s a lot of uncertainty out there and as noted on Tuesday, things are feeling increasingly stretched.

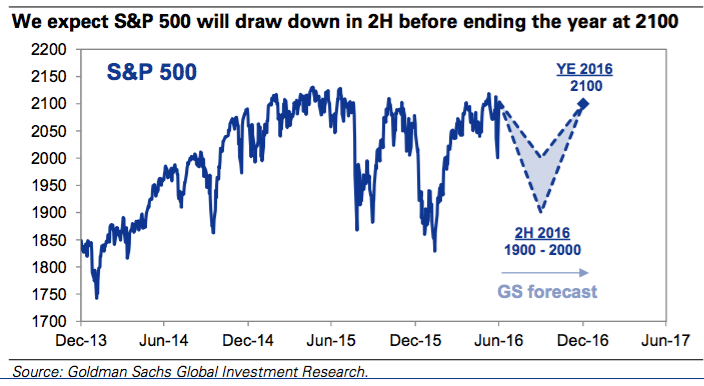

For their part, Goldman sees troubled waters ahead. “S&P 500 will continue to be range-bound during the remainder of 2016 [but] we expect a pullback of 5%-10%,” the bank said, in a note out yesterday. They even made a graph in case you can’t visualize that:

(Chart: Goldman)

For those curious, here’s the rationale:

“Although investors appear complacent in the wake of Brexit, a maturing economic cycle with elevated valuations, decelerating buybacks, and growing political uncertainty provide the basis for potential market weakness in the second half. “

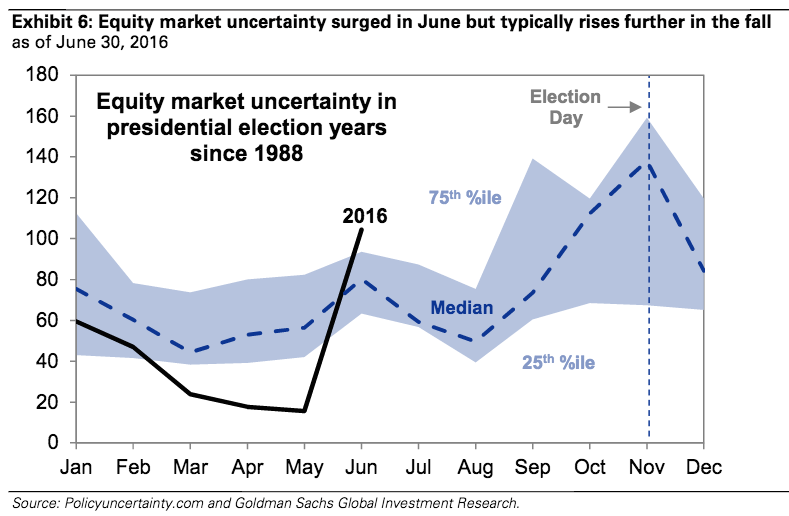

Note that these are all risks we’ve been cataloguing for months. There’s no demand for US equities outside of the corporate bid (i.e. share repurchases), valuations are stretched to the breaking point, and we’re coming up on an election that promises to make the political landscape in America even more divisive and contentious than it already is. Here’s a look at uncertainty in election years:

(Chart: Goldman)

And yet after a brief 8 sigma Brexit spike, the VIX simply threw in the proverbial towel and stopped caring altogether:

Ask yourself this: is that the appropriate level for the so-called “fear gauge” going into what BofAML is calling “the most important jobs number of the year”? Probably not. Here’s an excerpt from the bank’s latest:

“In our view, Friday’s US payrolls report will be watched even more keenly than usual as investors look for confirmation that the weak print last month was an outlier and not the start of a new, weaker trend. Market expectations are for a significant bounce to 180k, matching our economists’ estimates, but looking at historical data, we find some evidence of a tendency for consensus to over-estimate the size of the rebound following particularly disappointing payroll reports. With Brexit spillovers keeping markets nervous, we believe the risks around Non-farm Payrolls (NFP) are asymmetric, especially following the broad risk rally we have seen up until Tuesday this week, with a miss in payrolls likely to see risk sentiment sharply affected.”

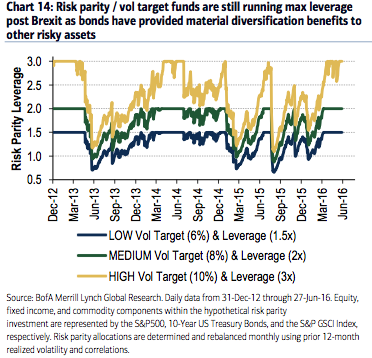

Of course that’s what you would have thought going into Brexit too. Keep in mind though, persistent strength in bonds likely mitigated the extent to which systematic strategies were forced to deleverage following the UK referendum, so one wonders if those chickens will eventually come home to roost following another “unfortunate” macro event:

(Chart: BofAML)

Having said all of that, remember that last week’s sharp bounce off the post-Brexit lows was a “bad news is good news and terrible news is even better” rally.

Perversely then, a bad jobs number on Friday could be just what the doctor ordered for risk.

Recent Comments