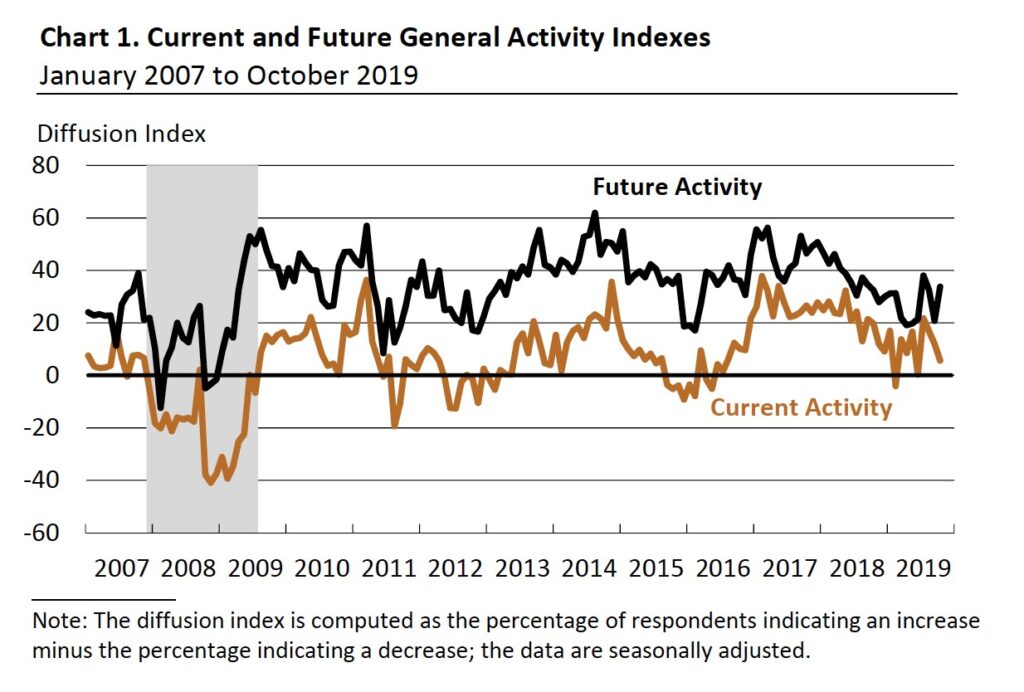

Philly Fed Index Falls, But Expectations Improve

Latest trend in the October regional Fed manufacturing reports appears to be positive, near zero readings. But an improvement in the expectations category which was hammered in the previous month. This trend worked for the Philly Fed report. As you can see from the chart below, the general business conditions index fell from 12 to 5.6 which missed estimates for 7.1.

Keep in mind, that the regional Fed indexes have been much stronger than the ISM manufacturing PMI. This reading is better than the September PMI. Economists thought the index would be even higher. That’s not in tune with the first yearly decline in industrial production since November 2016.

Specifically, the new orders index rose from 24.8 to 26.2. Shipments were down from 26.4 to 18.9. As I mentioned, the 6 month expectations index was the reverse as it rose from 20.8 to 33.8. This could be because of noise or optimism on the potential for a trade deal. Even though we’ve mostly seen soft data reports weaker than their hard data counterparts, this manufacturing survey oddly shows a lot of optimism for an economy in an industrial production slowdown.

In the expectations section, new orders rose from 35.2 to 39.9 and shipments increased from 41.3 to 42.9. Capex index increased from 25.9 to 36.4. As you can see from the chart below, that’s one of the best readings in the past 19+ years. Only 5.7% of firms see a decline in capex in the next 6 months. This isn’t much of a manufacturing recession if that’s accurate.

Disappointing Housing Starts

September housing starts missed estimates. This doesn’t signal another slowdown in housing, but it is a minor setback for a category which was expected to be rolling on all cylinders. Housing and consumption growth need to be great to avoid Q3 GDP growth having a one handle. That hasn’t happened which means it’s more likely than not that growth will be below 2%.

Specifically, housing starts were 1.256 million which is down from 1.386 million. It missed estimates for 1.3 million. Even so, starts were still up 1.6% from last year. Starts fell 9.4% from the previous month because in August, monthly growth was 15%. Single family starts were up 0.3% monthly (5th straight increase) and 4.3% yearly. They pack a more powerful punch than multi-family starts when it comes to GDP. Multi-family starts were down 28.2% monthly and 5.1% yearly.

Permits also fell, but they beat estimates. They fell from 1.425 million to 1.387 million which beat estimates for 1.335 million. Also, permits were up 7.7% yearly. Single family permits were up 0.8% monthly and 2.8% yearly. Multi-family permits were down 8.2% monthly, but up 17.4% yearly.

As you can see from the chart below, housing starts are correlated with permits pushed forward by 6 months. This implies starts will continue to improve modestly in Q4 and Q1. Housing is being helped by low interest rates and solid income growth. If either of those change, we could see it reverse course harder than in the 2nd half of 2018.

Finally, housing completions were down 9.8% monthly and 1% yearly. That’s readings of -8.6% and 1.8% for single family homes and -10.9% and -6.3% for multi-family homes. Looking at the regional data, the Northeast was a bloodbath for starts. But the strongest area for permits as yearly growth was -22.1% and 11.9% respectively. South, which is the largest housing market, had strength in both as its growth rates were 18.6% and 8%.

Redbook Sales Growth Weak Again

Redbook same store sales growth reading was very weak last week compared to the past few months of data. We’re used to seeing quicker Redbook sales growth than actual retail sales growth. If nominal retail sales growth ends up being 4.1%, like it was in last week’s Redbook report, that would be exactly in line with September’s report, meaning it wouldn’t be problematic. However, Redbook’s results have been above retail sales growth. So if the relationship continues, retail sales growth will fall next month. With that all being said, we can’t react too heavily to one week’s data because it can be noise.

Even though in the week of October 19th growth increased to 4.3%, this is still a negative in my eyes because it supports last week’s reading. I would have liked to see growth above 5%. The next weekly reading will be the final full week from October. October retail sales report doesn’t come out until Friday, November 15th. On the positive side, we’ve seen good consumer confidence results. This recent rally in stocks could help confidence slightly. A final October University of Michigan confidence index comes out this Friday.

Big Rebound In Richmond Fed Manufacturing Index

With the big improvement in the October Richmond Fed manufacturing index, the average of the regional Fed surveys shows the ISM manufacturing PMI should jump back above 50. I’m certainly expecting it to. The chart below shows the recent divergence. If the S&P 500 hasn’t already hit a record high, such an improvement in the PMI could catalyze a record. ISM PMI comes out on November 1st.

Specifically, the Richmond Fed index went from -9 to 8 which beat the high end of the estimate range which was -5. That’s right, no one predicted the index would be positive. Consensus was -9. In the index, volume of new orders increased from -14 to 7 and shipments increased from -14 to 4.

Furthermore, local business conditions increased from -15 to 4. There is no expectations index, but if it was weighted the same as the composite, it would have increased. Shipments and volume of new orders indexes were up from 15 and 22 to 24 and 33. Local business conditions improved from 5 to 12. On the negative side, capex fell from 19 to 7 and equipment and software spending fell from 21 to 4.

Recent Comments