Big Rally In Stocks After Strong Jobs Report

Many investors thought the November jobs report would show less jobs created than it did. And many also thought a very strong jobs report with high wage growth could be problematic for the stock market. I will review the headline numbers from this labor report later in this article.

It’s easy to get predictions wrong on a month to month basis. Intermediate term trends are more important. Declines in yearly job creation growth is clearly over. This signals the consumer will maintain its strength and there will be a strong economy in 1H 2020.

We’ve seen stocks react meekly to strong jobs reports in the past 2 years because of fears of inflation and rate hikes. However, the economy clearly isn’t overheating now as inflation has been falling. I should have realized a strong report would be great news because fears of a recession currently outweigh fears of rate hikes and inflation. The fact that the Fed funds futures market was pricing in a rate cut in 2020 before this report shows the direction markets were leaning in.

The stock market has had a great run in 2019, but bullishness in the AAII sentiment survey is low and over 60% of economists see a recession occurring in the next 2 years. Clearly, few are worried about inflation. We need to see a few strong inflation reports before wage growth is back to being a negative.

Nominal wage growth is below where it peaked last year when it made the 10 year yield spike. For the consumer, wage growth is strong because inflation has fallen, but for businesses it’s less of an issue. If we continue to see nominal wage growth increase, it could be an issue in early 2020, but we aren’t there yet.

Review Of Friday’s Nice Rally

S&P 500 was up 0.91% on Friday which put it just a few points away from its record high. The mini correction is over. Even though stocks were overbought at this level, I’m not bearish in the near term right now. You can’t be bearish with such a blowout jobs report even if it was helped a bit by the end of the GM strike. 2H 2019 was supposed to be the weak point of this slowdown. But we might not even see a sub 2% quarter over quarter GDP growth reading. I was correct to be more optimistic on Q4 GDP growth than many estimates.

This holiday shopping season looks like it will be good. There was never going to be a recession in 2019 in my view. Recession talk has finally been put to rest for good.

Nasdaq was up 1% and the Russell 2000 was up 1.18%. Stocks don’t even need a trade deal to rally because a cyclical upturn is upon us. VIX fell 0.9 to 13.62. CNN fear and greed index only rose 3 points to 70 which is greed.

This indicator doesn’t scream sell yet. It’s extreme greed readings earlier this fall didn’t work out well for the bears. Just because an indicator is wrong once, doesn’t mean I won’t use it anymore. Its long term track record is still solid.

Every sector rose except utilities which shows how the risk on trade dominated. Utilities were down 0.22%. The 2 biggest winners were the financials and energy which rose 1.35% and 2%. Financials were helped by the modest rise in treasury yields. I would have expected a bigger increase in yields based on how solid this jobs report was.

2 year yield increased 2 basis points to 1.61% and the 10 year yield rose 3 basis points to 1.84%. Financials love rising rates and a steepening curve. Odds of a rate cut by the March meeting fell from 24.8% to 20.8%. Oxford Economics see a cut by that meeting. I see no cuts in 2020 and 1 hike in 2021.

Strong November Jobs Report

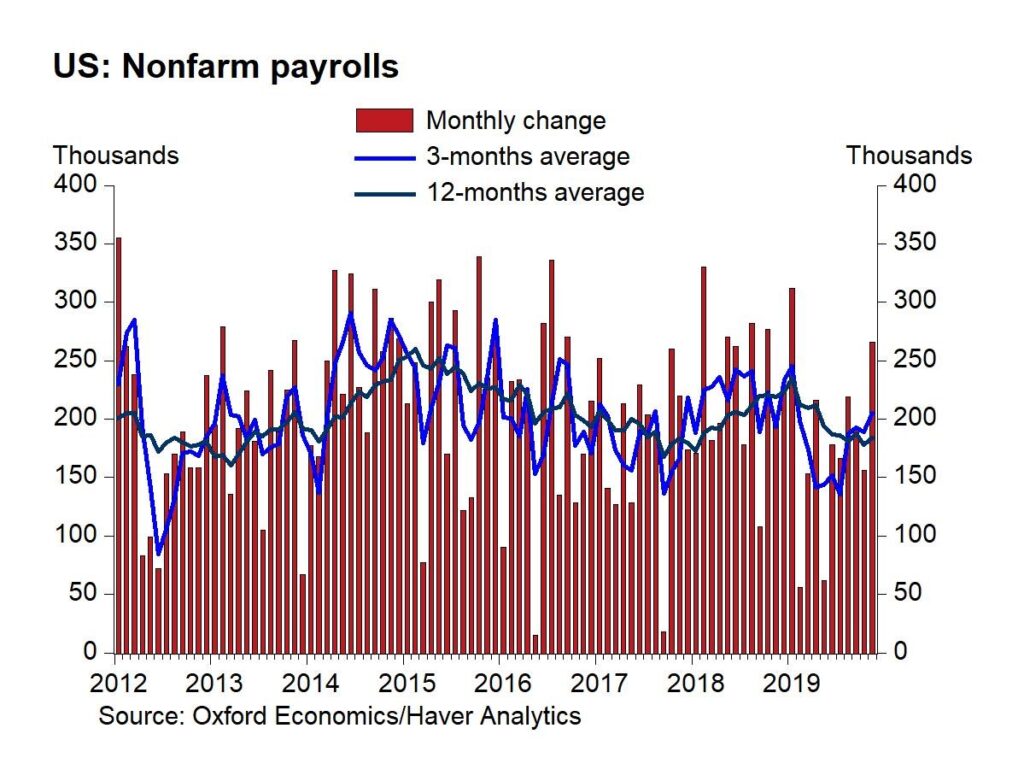

ADP report was way wrong as it was too negative. There were 266,000 jobs created which beat estimates for 180,000 and the high end of the estimate range which was 210,000. Private sector job creation was 254,000. It beat estimates for 168,000, the high end of the estimate range which was 200,000. And the ADP report which showed only 67,000 jobs added. It was helped by the end of the GM strike. That added 41,000 jobs. Even without that, this report would have beaten estimates.

As you can see from the chart above, the 12 month average of job creation increased to 184,000. It looks like it is bottoming. 3 month average increased to 205,000. Both were helped by the positive revisions. October report was revised to show 156,000 instead of 128,000. September reading was revised higher by 13,000 to 193,000.

Unemployment rate fell 0.1% to 3.5% which matched the cycle low. Besides the September reading, this is the lowest rate since December 1969. Underemployment rate fell 0.1% to 6.9% which also matched the September low. Lowest rate ever was 6.8% in October 2000. Finally, average hourly wage growth fell from 3.2% to 3.1% which beat estimates for 3%. It increased from the original October reading which was 3%.

Conclusion

Labor report beat estimates even excluding the GM strike effect. Labor market is strong. It appears the consumer will also be strong in Q4. That will allow GDP to avoid the dire forecasts of below 1% growth. It was wrong to worry about stocks being hurt by high wage growth. Inflation isn’t a concern yet. Wage growth isn’t as high as it was in 2018.

Recent Comments