Before I get into a discussion of the latest market action, I will make a clarification of an aspect which I wasn’t aware of. As I have mentioned a few times in the past few weeks, the NY Fed’s Nowcast Q1 GDP growth estimate and the Atlanta Fed’s Q1 GDP Now growth estimate are far apart. Currently the NY Fed model is forecasting 2.8% growth in Q1 and the Atlanta Fed model is projecting a meager 0.6% growth rate. I stated I didn’t have the data on past instances when they diverged to determine which model is likely to be more accurate. The historical data wouldn’t matter as each quarter is different. The better way to determine which model is going to be more accurate is to look at why they are differing.

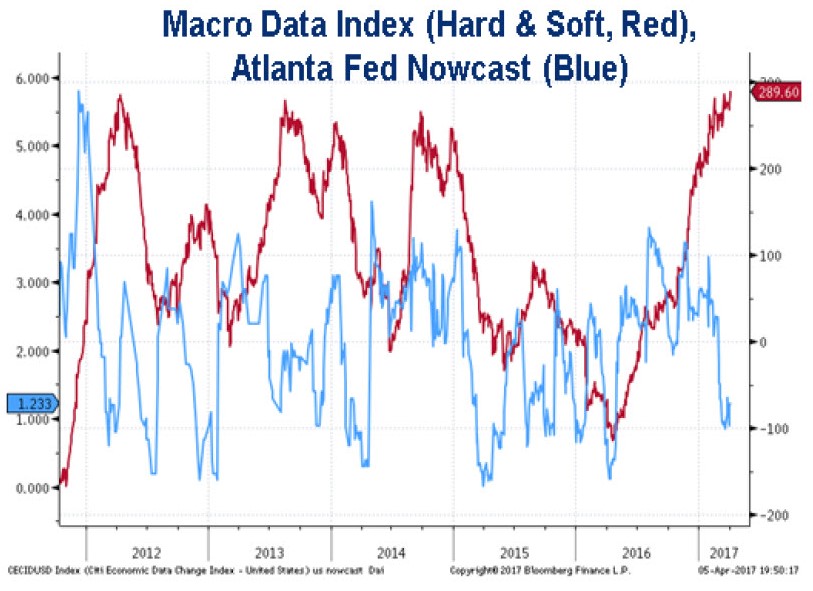

The reason they are differing is because the NY Fed tries to link econometrically soft survey data like consumer confidence, ISM, and the Philly Fed, to a GDP estimate. The NY Fed model includes a much larger percentage of linked estimates from soft data than the Atlanta Fed’s model does. The chart below shows the recent large gap between the soft data and the Atlanta Fed’s forecast. We are once again back to battle between soft and hard data. There is no way to prove whether the soft or hard data will be correct in predicting medium term growth, but for this quarter, the Atlanta Fed will be more accurate since sentiment has no weighting in the GDP report. The one thing sentiment effects is how the market responds to the GDP report. The next report will be weak, so it will be one of the toughest challenges the bull market will face since the start of the year.

Moving into the market’s action on Tuesday, the ten-year bond yield fell sharply to 2.299%. The yield is now down 6.64% year to date. The increase in the yield from the all-time low of 1.3180% may have been a head fake. The reflation trade isn’t working as long-bond bears who were betting on the improving sentiment indicators are paying dearly for their miscalculation. Tying in with the earlier point, the rally in the ten-year bond is consistent with the Atlanta Fed’s forecast for low growth in Q1. The chart below shows the bullish case for equities as the bulls are expecting investors to rotate money from bonds into stocks. That certainly hasn’t happened lately. The increase in both since 2009 gives you a taste for how much liquidity is sloshing around. If there is a rotation into stocks, record PE multiples may result.

The chart below shows the flow of investors’ money back into long term bonds. The short trade on long bonds became very crowded in the beginning of the year. That trade has now unwound itself as hedge fund managers are approaching no longer having a short position in long bonds. To clarify, the trade unwinding is not happening because it was crowded; it is unwinding because hard data has weakened. However, the speed at which yields have fallen is a result of it being crowded. This is a warning for bullish stock investors. The fact that everyone and their mother is in stocks could set up a quick dip lower when the fundamentals start to deteriorate further.

Those on the bearish side of long bonds would argue with the assertion that long bonds were overbought. As you can see from the chart below, the duration of the Barclays global aggregate index is at its all-time high. Bonds have never been riskier and have never provided such low returns. This a long-term trend which has been driven by decelerating productivity and labor force growth in the developed world and the asset purchases of global central banks. Betting on bonds is a bet that inflation will remain subdued.

The other major move in the market has been rising oil prices. Oil is up from the high forties to a $53 handle. One of the latest driving forces for oil has been the American airstrike on Syria. The fact that it’s being done by a new president adds to the uncertainty. If the situation calms down without any more actions in the next few days, expect oil to fall back closer to $50.

The second reason oil fell is because of the latest news coming out of OPEC about the production cuts. OPEC and non-OPEC nations have adhered to production cuts. The eleven nations who agreed to the cuts averaged 29.804 million barrels of cuts per day. This represents 104% compliance as the goal was 29.757 million barrels of cuts per day. When you include Libya and Nigeria, two nations not part of the eleven who were part of the deal to cut production, production fell 31.939 million barrels per day. That’s 19,000 lower than last month. OPEC and non-OPEC nations had a combined compliance of 94% in February. This is expected to increase in March.

As I mentioned the uncertainty created by the Syrian airstrikes increased oil prices. This uncertainty didn’t hurt stocks even though it raised tensions between America and Russia. It’s not a surprise that political uncertainty was ignored as that’s been a growing trend with the stock market rising despite the global rise of populism which tends to be against free trade. The charts below show this situation playing out as the VIX had its second lowest quarter ever in Q1 and the Global Economic Policy Uncertainty Index remained high. The final chart shows how one-month realized volatility is also very low.

Conclusion

The latest moves I discussed in this article are the declining yields in long bonds, rising oil prices, and the incredibly subdued VIX. I also mentioned that the Atlanta Fed GDP model forecast of 0.6% growth is likely to be more accurate than the NY Fed model because it puts less emphasis on survey data. We’re at the point in the quarter where the Atlanta Fed model is as accurate as it gets. I doubt the model will show much movement in the days leading up to the April 28th report.

Recent Comments