Extreme Fear Continues

The S&P 500 fell 4 basis points. Dow rallied 0.26% because Proctor and Gamble beat earnings estimates. This caused its stock to increase 8.8%.

The Nasdaq fell 0.48% and the Russell 2000 fell 1.2%. Advanced Micro Devices was the biggest loser in the S&P 500 as it fell 11.1%. The best sectors were consumer staples and utilities which increased 2.31% and 1.68%.

It’s tough to say if Proctor and Gamble stock rose because of great earnings or because defensive names are popular now.

Their EPS beat estimates for $1.09, coming in at $1.12. Revenues of $16.69 billion beat estimates by 0.8%.

Those seem like normal results for this firm, yet its stock rallied sharply. I think traders are piling into these consumer staples names any chance they can. The worst sectors were healthcare and energy which fell 0.95% and 0.89%.

It’s interesting that even though the Nasdaq fell, the tech sector was up 1 basis point.

Possibly, the negative housing data is scaring Wall Street. It’s a new catalyst to consider besides earnings season and the Fed.

Furthermore, small caps must deal with rising rates as over half of Russell 2000 firms’ debt has floating rates.

New negative catalysts are emerging constantly which makes me more pessimistic on intermediate term returns. I’m still bullish on the short term though. The CNN fear and greed index is at 14 out of 100 which means extreme fear.

Extreme Fear - Fearless Consumer

The concept of extreme fear in the stock market needs to be explained. There’s obviously not capitulation level fear like at the end of a bear market.

This is simply very short term fear which usually accompanies a correction. As I mentioned, even if this isn’t a correction and it is a bear market, stocks should rally temporarily. They are oversold.

The extreme short term fear isn’t consistent with consumer confidence seen in the chart below.

That’s good news for GDP growth and the stock market. It means consumer spending should be strong this holiday season.

Historically, the savings rate has gone down when household assets have increased. But in this cycle the savings rate has remained elevated and consumers have deleveraged.

Since consumers aren’t relying on wealth growth, it’s interesting to consider how much a decline in the stock market would affect spending. It would probably have some impact. Just not as much as if consumers spent as if that money would be available.

Those who are retiring the soonest and have the most money in stocks would be hurt the most by a correction. It’s a risky point in the cycle to have money in stocks if you need it within 5 years.

Extreme Fear - Hawkometer Turning Red

Fed’s hawkishness in the face of this correction shouldn’t be surprising. The stock market has needed to fall 12.5% since the financial crisis for the Fed to react.

There is a possibility the Powell led Fed is more resistant to stock market corrections. The idea that the Fed will hike until something breaks is dangerous. Cracks can appear quickly once the stimulus stops boosting the economy.

The housing market already looks weak even though the 30 year rate is only at 5%.

That’s much higher than last year, but not the highest of this cycle. Existing home sales have fallen 6 straight months. This has happened 3 other times in the past 20 years. Those are January 2004, October 2007, and December 1999.

The one in 2004 was the only situation where housing kept increasing in the intermediate term. This could be another situation where housing recovers. However, there’s less of a chance of that occurring if the Fed gets more hawkish.

Currently, there is an 83.9% chance the Fed raises rates at least 1 more time this year. The Fed’s Kaplan recently stated 2 or 3 more hikes might occur by June 2019.

That’s basically in line with the Fed fund futures market. There is a 78.9% chance of at least 2 hikes by June and a 37.3% chance of 3 more.

As you can see from the chart below, the number of times the Fed has used variations of the word ‘strong’ in its Minutes has increased ever since Powell took the helm. The Fed appears to be ready to hike rates above the long run rate.

Extreme Fear - Earnings Season Looks Good

The biggest reason this will probably be a correction and not the start of a bear market is earnings still look good. Earnings have saved the market.

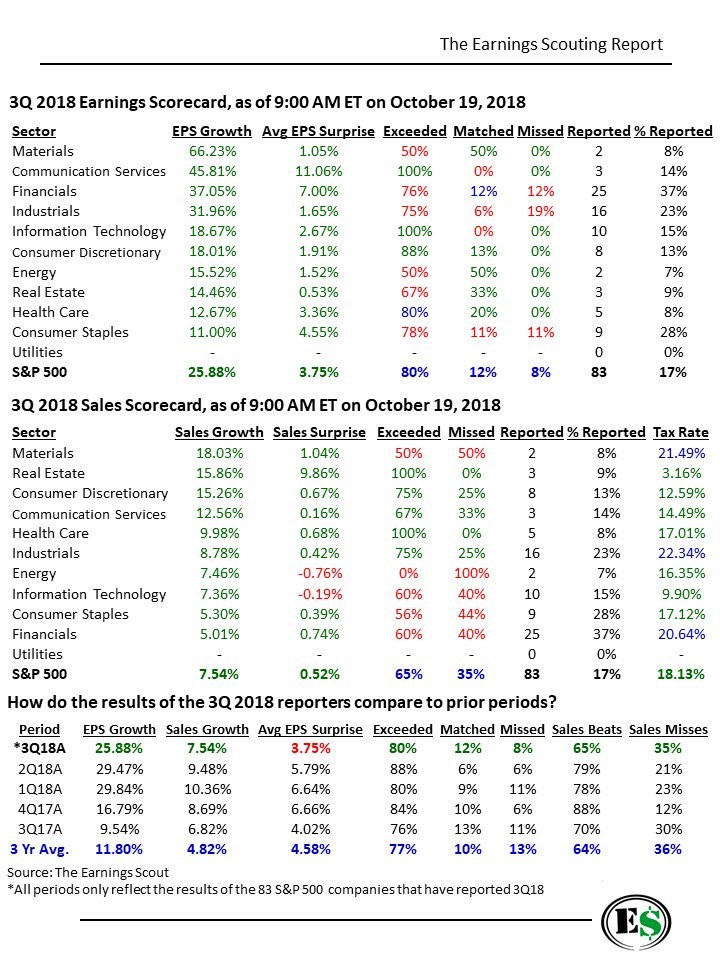

As you can see from the table below, the first 78 firms in the S&P 500 have reported EPS growth of 25.88% and revenue growth of 7.54%. The average EPS surprise rate isn’t great at 3.75%. Average revenue surprise rate is subpar at 0.52%.

Communication services sector has started off on the right foot. 100% of firms have beaten EPS estimates with an average beat of 11.06%.

Since Q3 earnings growth was always expected to be the highest of the year, the estimates started out really tough.

This explains why they fell heading into earnings season unlike the past 2 quarters. And also why the average surprise rate is 2.04% lower than last quarter.

With earnings growth of 4.04% below the pace set in Q1, it’s unlikely that this quarter will catch up. We must respect the great numbers and not fear the below average beats. That is, unless they cause earnings estimates in future quarters to decline.

As you can see from the chart below, Q4 earnings growth is still expected to be 15.01%. There will be less margin for error in 2019. Q1 2019 EPS growth is starting out at 8.47% and Q2 is at 6.39%.

Sustained economic weakness can easily pull them to the flatline. Investing in the stock market appears risky next year. At best it appears stocks will rally in the high single digits and at worse there will be a bear market.

The upside is capped and the downside scenario is growing increasingly likely.

Recent Comments