Goldilocks Sends Stocks Higher

The stock market soared on the Goldilocks jobs report on Friday. Investors were curious how the market would react to weakness. Apparently, the market is fine with slowing payrolls growth. It’s not necessarily a new trend, but weakness in manufacturing wasn’t a new trend. Yet stocks fell after the weak ISM report. The market is acting so jittery in both directions. Even if you knew the data beforehand, you wouldn’t be able to predict short term moves. I will finish off explaining the BLS report later in this article.

Friday’s Big Rally

S&P 500 loves staying near 3,000 so much it had to rally Thursday and Friday. It increased 1.42% to 2,952 on Friday. Nasdaq increased 1.4% and the Russell 2000 rose 0.97%. VIX fell 2.08 points to 17.04. It’s amazing how many shifts there have been in the first week of October and we didn’t even get to the major news of the month. Big events will be in the next 2 weeks as earnings season gets going, the Democrats debate, and America has trade meetings with both Europe and China.

CNN fear and greed index only increased 3 points to 32 which is fear. Just like on Thursday, every sector increased. Every day in October has seen every sector move in the same direction (first 2 days down & second 2 up). Biggest winners were technology and financials which rose 1.71% and 1.93%. The market doesn’t appear to be worried about the weak Q3 GDP growth reading coming because it doesn’t see a recession. Personally, I agree.

It will be interesting to see how much the Fed’s 2019 rate cuts help the economy next year. There is currently a 76.4% chance of a rate cut in October. Even though the odds of a cut didn’t go up, I think traders were just happy that the recent dovish move in the Fed funds futures market stayed in place. Treasury yields stayed low as the 2 year yield increased 1 basis point to 1.4% and the 10 year yield fell 1 basis point to 1.53%. 10 year yield is only 10 basis points above its 2019 low.

Big Decline In Wage Growth

One of the biggest stories about the September jobs report is that hourly wage growth fell. Monthly wage growth was 0% which fell from 0.4% and missed estimates for 0.3%. It’s surprising to see such low wage growth with the labor market still nearly full.

Good news for workers is headline CPI has been weak. In August, headline CPI fell about 6 basis points to 1.76%. That’s even though its comp fell 27 basis points. If the cyclical weakness continues, CPI will fall further. The economy certainly isn’t overheating.

As you can see from the chart below, average hourly wage growth fell from 3.2% to 2.9% which missed estimates for 3.2%. That’s the lowest hourly wage growth since July 2018. Since the work week stayed at 34.4 hours, which met estimates, weekly wage growth fell from 2.9% to 2.6%. It’s the weakest growth since October 2017.

Good news for most workers is average hourly wage growth for production and non-supervisory workers only fell 10 basis points to 3.46%. This was only the weakest reading since this June. Non-supervisory workers are doing fantastically given the low inflation rate. Usually, these workers do the best at the end of the cycle.

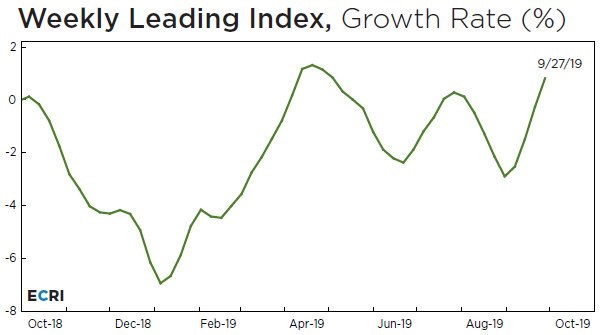

Easy Comps Help Leading Index’s Growth Rate

We are now in the period where easy comps will start to drive the ECRI leading index’s growth rate higher. That’s what occurred in the week of September 27th as you can see in the chart below.

Weekly index fell from 146.5 to 146.1, but the yearly growth rate rose from -0.3% to 0.8%. With easier comps, I expect growth to get to the mid-single digits in Q4 which will be the highest growth rate of the year. This won’t turn me extremely bullish on a cyclical turnaround. I need to see the nominal index increase to get optimistic.

Weak Q3 GDP Growth Reading All But Assured

Advanced Q3 GDP growth reading will be released on October 30th. I’m very confident quarter over quarter real GDP growth will be below 2.5% as the estimate range is from 1.5% to 2.7%. Average and median estimates are 1.7%. On Friday, the Atlanta Fed Nowcast updated to show 1.8% growth which was the same as it was on October 1st.

Increased expectations for real personal consumption expenditures and real government spending growth were offset by declines in estimates for real gross private domestic investment and real net exports.

Decline in the Q3 NY Fed Nowcast wasn’t as bad as the decline in the average estimate as it fell 3 basis points to 2.03%. ISM manufacturing report had the biggest impact on the NY Fed’s estimate as it caused it to fall 9 basis points. Improvement in the unemployment rate and the number of employees helped the estimate by 4 basis points.

While the Q3 Nowcast didn’t move much, the Q4 Nowcast fell sharply from 1.76% to 1.3%. That’s still not its lowest estimate for Q4. I’m interested to see if the economy rebounds in Q4. There’s not much room left for the economy to fall before it hits recessionary levels. St. Louis Fed is one of the few estimates above 2.5% as it is at 3.12%. I don’t believe it will be correct.

Conclusion

Stocks rallied on a somewhat disappointing jobs report because it signaled the economy wasn’t recessionary, but was weak enough for more Fed rate cuts. While the economy won’t hit a recession this year, it’s surprising to see such optimism.

Q3 is on pace to have very weak GDP growth. Q4 could be weak. But it depends on how the trade negotiations between China and America go next week. A deal would cause management teams to invest more because they would gain visibility.

Recent Comments