Remember what we said two days ago about “expectations?” They can be dangerous things.

Going into Friday’s BoJ decision, expectations were in fact running so high it wasn’t even clear what they were. ”If the BOJ doesn’t move this time, there’s a possibility that the yen will strengthen further,” Hiroaki Muto, chief economist at Tokai Tokyo Research Center in Tokyo told Bloomberg headed into the drama.

Of course we all knew the yen was going higher (i.e. Stronger) regardless. There was no way they could have made a splash. That would have entailed another 20 bps in rate cuts, a bazooka for the ETF purchases. And some kind of coordinated message with Abe to suggest what role the bank will play in fiscal stimulus.

Here’s what we got instead:

* Kuroda expands ETF target purchases to 6t yen, and orders assessment of effectiveness of BOJ policy for Sept. meeting

* The BOJ maintained policy interest rate at -0.1%

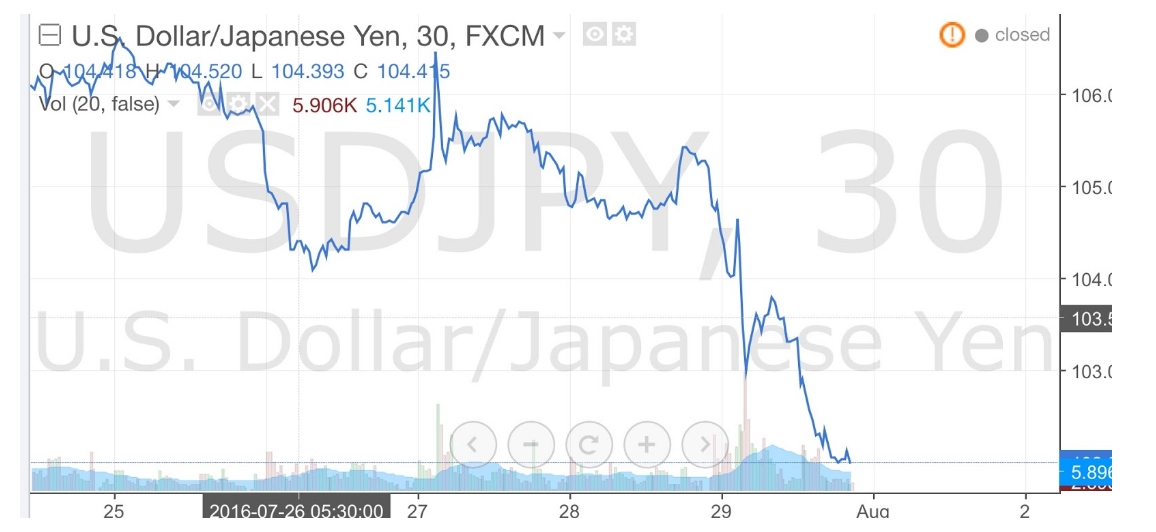

* USD/JPY just under 2% to 103.30 after falling as low as 102.71. Yield on 10-year JGB jumps 9.5 bps to -0.18%, set for the steepest advance since 2013

* USD/JPY 3-mo. basis swap climbs 5.6 bps to -65 bps

* Macro accounts sold USD/JPY after a muted rally following BOJ’s decision, with some clients already expecting BOJ to disappoint beforehand, trader says

“The message the BOJ is sending is not so much ‘whatever it takes’ as monetary policy’s pretty much played out, SocGen said, adding that nothing here to weaken the yen.”

Well thanks SocGen, that’s pretty dark. “That was rather half-way, wishy-washy” another analyst quipped. Needless to say, the yen rallied hard

Now you’d think that would have led directly to a rather nasty carry unwind, but after a harrowing session, the Nikkei managed to pull out a green close. Europe was green as well and in the US, Alphabet and Amazon’s quarters were enough to keep us afloat despite a lackluster GDP print.

Clearly what’s interesting here is the combination of the lackluster set of measures and Kuroda’s explicit directive to assess the effectiveness of the policy?

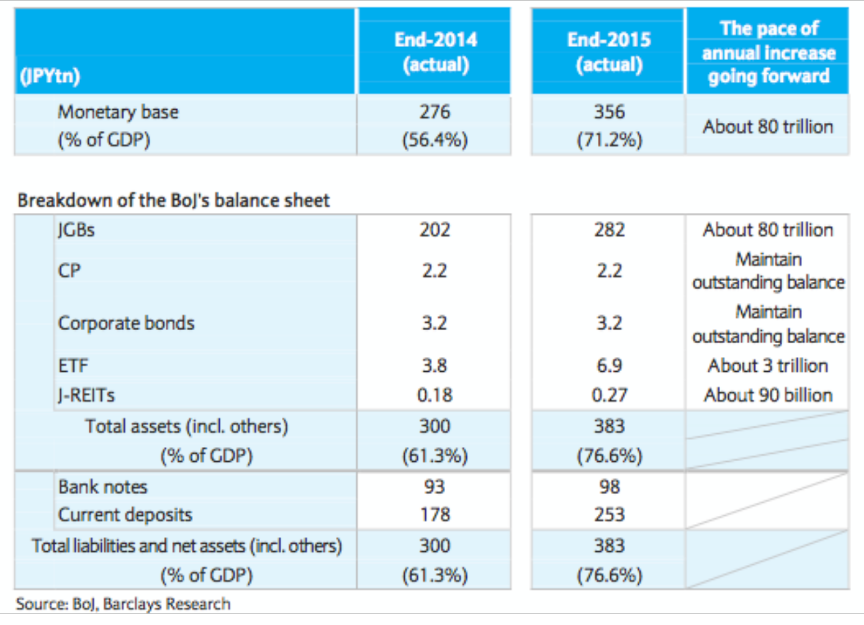

One certainly wonders if this might be the beginning of the proverbial end. They seem very reluctant to go further into negative rates and if you needed any more evidence about just how precarious the Japanese government bond market has become, note that the primarily dealers are starting to resign. As for the ETFs, you’re reminded that Kuroda already owns 55% of the entire market. For those who missed it here’s the diagram via Barclays.

Surely the BoJ won’t be the first to admit defeat. In the meantime we would note the BoJ is already a top 10 holder in 90% of the Nikkei – looks like he’s going to flat out corner it.