It is always important to invest with the macroeconomic back drop in mind. However, this concept is actually hurting investors this year. In fact, not only is economic weakness not being priced into the market, but individual earnings reports aren’t mattering either. Capitalism cannot work when there is no cost of capital. Investors begin to look at firms differently because it is so cheap to borrow money. Firms that borrow money to fund growth are valued the highest.

The worst companies having the best stock performance is nothing new. In the 1990s tech bubble, stocks which had no earnings were rallying faster than firms with consistent business models. In the current situation consistent dividend payers are in a bubble because they are the only game in town given how low government and corporate bonds yields are. However, the bubble in dividend stocks (particularly consumer staples) pales in comparison to the one in the momentum stocks which make up TFAANG (Tesla, Facebook, Apple, Amazon, Google, and Netflix).

The king of the momentum stocks is Netflix. Netflix represents exactly what speculators crave in this market. They want to see growth at any cost. They believe that market share is more important than profits because after the customers are acquired, the firm can begin to raise prices and become a cash cow. This ignores the difficulty Netflix has already had with raising prices in the past. Last year’s price increase was put through so gradually Netflix had to invent a new term called “un-grandfathering.” This is when existing customers which got to pay the previous lower price after the price hikes effect new customers lose this privilege. 75% of the “un-grandfathering” had occurred by the end of the last reporting period.

It makes sense that Netflix values its existing customers higher than new customers as they have been paying for the service which makes them more likely to stay. However, the grandfathering process which keeps prices lowered for longer for existing customers is money that could have been spent towards acquiring new customers. Momentum speculators believe Netflix is this growth engine which has the ability to grow total subscribers without effort. However, if Netflix is having a tough time keeping its existing customers, this thesis seems doubtful.

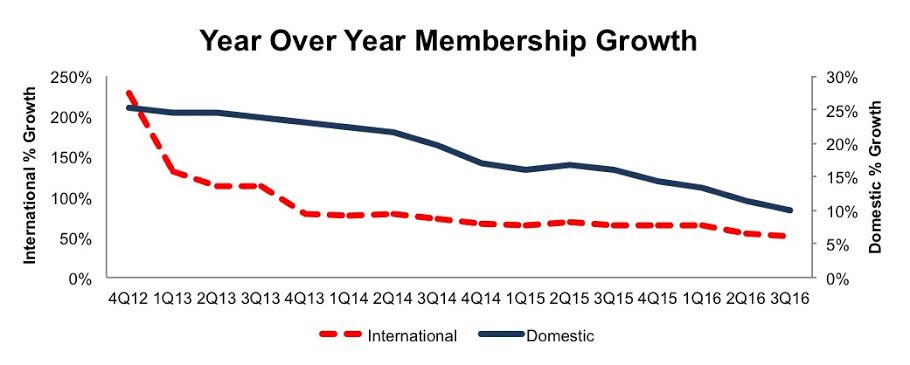

The chart below is evidence of this slowing subscriber growth. Even though the company is spending more cash than it takes in, it can’t keep its subscriber growth rate from decelerating. The company is a perfect microcosm for the global economy. Even as fiscal deficits skyrocket out of control and interest rates are at all-time lows, the economy is tapped out and cannot grow any longer.

Because of the spending by Netflix on original programming to chase after a less and less new subscribers, the firm had a record negative free cash flow of $506 million. Even as the company burns cash to acquire customers which will leave it when it does raise prices to a level where acceptable profit margins are achieved (may be a $4 increase), debt investors can’t get enough its bonds.

Netflix had so much demand for its senior notes which yield only 4.375% that it upsized its offering from $800 million to $1 billion today. S&P correctly rates this bond offering as B+ which is junk level. The market is in a “risk on” mode as investors are buying assets with the intention on getting out before the sentiment turns.

Netflix stock trades at 122 times 2017 earnings (which were recently revised higher because of the subscriber growth beat this past quarter). This valuation can’t be justified by rational logic. I point it out to show how investors are ignoring profits.

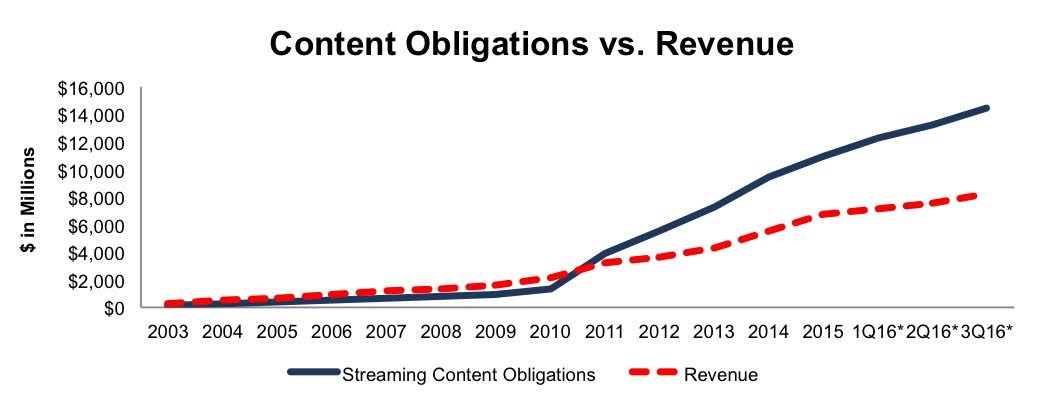

Because we are at the end of the business cycle, growth is harder to come by as profit margins have peaked. This makes companies that can grow revenues even more valuable. This partially why Netflix stock is near its all-time high. Investors are ignoring the content obligations which are skyrocketing as shown in the chart below. This spending increase reminds me of the U.S. government’s reckless spending. Considering the U.S. government would be bankrupt if it couldn’t print money, this is a scary comparison for Netflix. Netflix won’t be able to issue shares and debt for as long as the U.S. government has printed money.

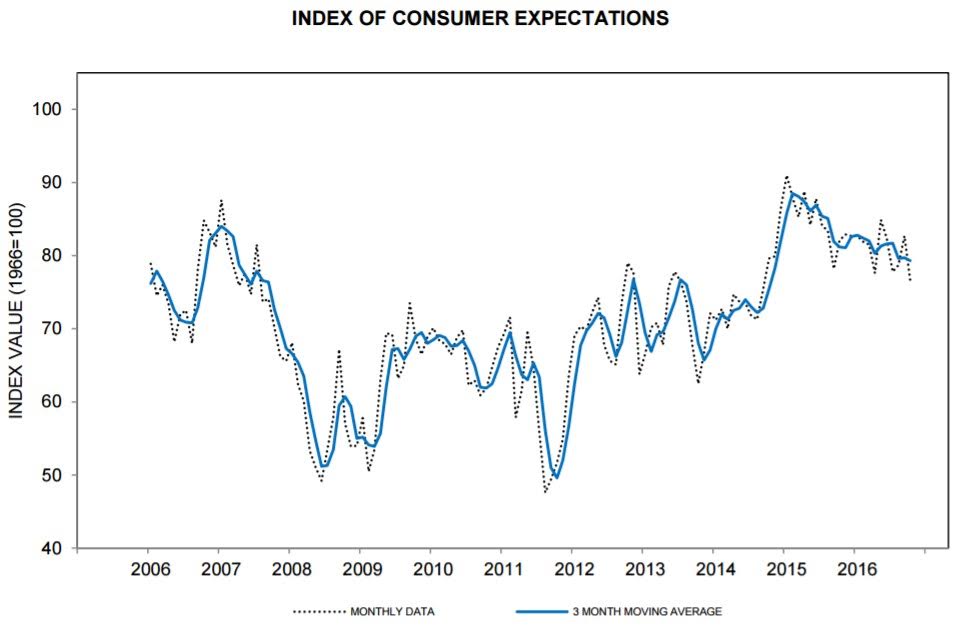

The chart below shows consumer expectations. As the business cycle rolls over, the consumer sentiment will continue to fall further off its peak. This makes Netflix price increases even more difficult to execute without increasing its churn rate. Netflix stock is riding high even as it is about to go through a tough period where not only will U.S. subscriber growth slow, but the total may even contract.

Conclusion

The stimulus provided by monetary policy has diminishing marginal returns. Each round of QE provides less economic growth as the debt level drags the economy lower. This stimulus is what is causing Netflix stock to rise while its cash flow plummets. It also provides an analogy for our current economy as decelerating subscriber growth causes the stock to rise as expectations are so low. The stock market as a whole and Netflix in particular cannot not keep rising along with slower growth. Usually stocks like Netflix transition from growth to value stocks when growth slows. This would be a painful transition as investors would actually take the cash flow and earnings seriously. Netflix stock needs to be avoided like the plague.

1 Comment

Ali Alhaschemy

October 25, 2016Great Job Theo.